Viagra gibt es mittlerweile nicht nur als Original, sondern auch in Form von Generika. Diese enthalten denselben Wirkstoff Sildenafil. Patienten suchen deshalb nach viagra generika schweiz, um ein günstigeres Präparat zu finden. Unterschiede bestehen oft nur in Verpackung und Preis.

Building.co.uk

13/CLIENT INTELLIGENCE 2013

CLIENT INTELLIGENCE 2013

2/executive summary

6/top client lists

6.1 Top 50 public and regulated sector clients

6.2 Top 50 private sector clients

3.1 Methodology3.1.1 Surveys

7/top 15 public and regulated sector client profiles

3.1.2 Public/private split

Basildon District Council

3.1.3 Top client tables and factfiles

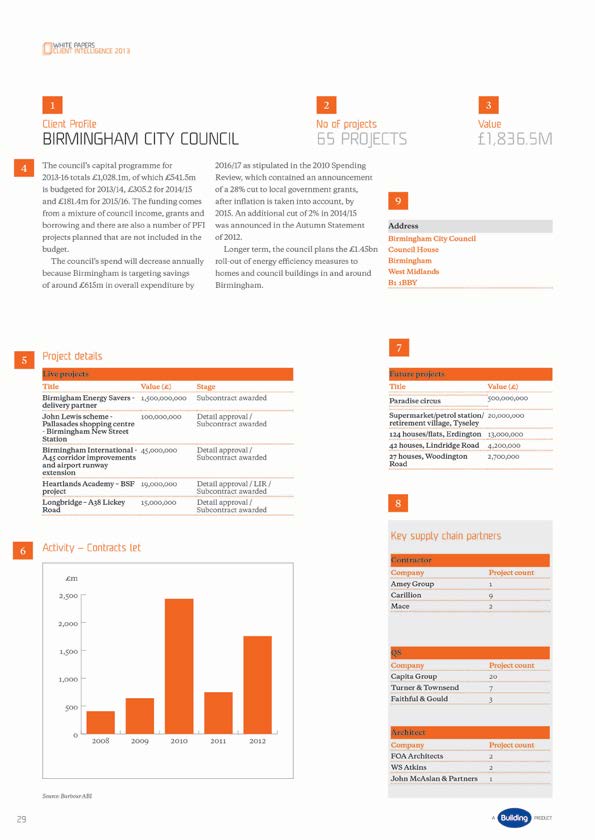

Birmingham City CouncilCrossrail EDF Energy

4/market overview and key sector breakdown

Essex County Council

Glasgow City Council

4.1.1 Private housing

4.1.2 Public/social housing

Homes and Communities Agency

4.2 Public sector building

Kent County Council

Ministry of Defence

4.2.3 Other central and local government

4.3 Private sector building

South Tyneside Metropolitan Borough Council

Sunderland City Council

Transport Scotland

4.3.3. Industrial4.3.4 Leisure and other private sector building

8/top 15 private sector client profiles

4.4 Infrastructure

4.4.2 Energy, airports and communications

Covent Garden Market Authority

4.4.3 Water, harbours and flood defence

4.5 Repair and maintenance

Gallagher Developments

4.5.1 Residential

4.5.2 Non-housing

4.6 Regional spending predictions

Legal and General

4.7 Further market trends

Lend LeasePeel GroupSainsbury's

5/client sentiment survey

5.2 Selection processes

5.4 Payment5.5 Qualities sought 5.6 Innovation

9/appendix: list of key supply chain partners

5.7 Government policy

by value of project

CLIENT INTELLIGENCE 2013

2/ExEcutivE summary

The last 12 months have seen little change

l

The majority of private clients are

in the raft of difficult issues facing UK

optimistic about starting or restarting

The research shows that the

construction clients. The economy has

projects put on hold this year. The survey

private sector's distaste for

been bouncing along the bottom, unable

found 58% of private clients are set to start

using frameworks to procure

to decide between recession or growth, but

projects, up from 50% in 2012.

with continuing funding constraints for the

construction services has only

private sector and cuts in public sector capital l

Public sector clients are more focused on

deepened over the past year

spending, construction output fell by more

cost than ever before: price has become the

than 8% in 2012.

most significant factor when choosing a

The findings of Building's second Client

contractor for 38% of public clients, and the

Intelligence white paper show that intense

use of "target price" contracts, which share

followed by price and financial stability – but

difficulties remain in obtaining approval to

price risk, has halved.

a far higher proportion of public sector clients

go ahead with major construction projects,

said price was the key determinant than last

because of continued difficulty acquiring

l

Payment times in the public and regulated

year. Interestingly the same isn't true for the

development funding and the uncertain

sectors have improved, with more than

private sector, for whom the priorities have

economic outlook.

60% paying within 30 days. However,

barely changed.

However, the findings also show the first

major payment problems remain in the

Sustainability seems to have fallen

signs of a nascent recovery in the private

private sector, with 46% taking more

further down the pecking order, with far

sector: more private clients are expecting to

than 30 days.

less government focus on the issue than

be able to restart projects than at this time

under the previous administration. While a

last year – more than half of all of those

l

The overwhelming majority of clients still

contractor's track record on sustainability

surveyed. But, with the public sector more

make use of retention payments – 77% in

remains a low priority for both public and

price-conscious than ever, the research

both the public and private sector.

private clients, the number that report using

is clear that a significant turnaround in

"whole life costing" in their procurement is

workload is not an immediate prospect.

l

The private sector is ahead of the

sharply down on last year. Both public and

According to our research for this

public sector in the use of both BIM and

private clients say more leadership is needed

white paper, which included a survey and

project bank accounts, with more than

from government to justify the investment

interviews with over 300 construction clients,

twice as many private clients using project

in sustainability, with nearly two-thirds of

there are a huge range of issues preventing

bank accounts, and 46% using BIM,

private clients supporting the roll-out of

work from starting. General macro-economic

compared to just 36% of public clients.

display energy certificates to private sector

uncertainty is the biggest problem for

private sector clients, while three-quarters

The research shows that the private sector's

still say it is difficult or impossible to access

distaste for using frameworks to procure

development finance – exactly the same

construction services has only deepened over

proportion as last year. The government's

the past year, with the proportion saying

austerity programme is also blamed for

they had used frameworks in the last year

making the problem worse, with four times

dropping significantly. By far the majority

as many clients saying it is worsening

of private clients predominantly procure by

confidence than improving the situation.

inviting selected contractors to compete.

More than half of public and regulated

Meanwhile, the public sector's method

sector clients report that construction

of procuring, predominantly through

budgets have been cut since 2010, with more

frameworks, has barely changed. This and

than two-fifths expecting budgets to be cut

other data tends to give weight to last year's

again before the end of the parliament.

finding that contractors shouldn't expect

This has seen the public sector refocus

major changes in the way public clients

on price. On average, both public and

procure following the implementation of

private clients see build quality as the most

the government's Construction Strategy.

important factor when selecting a contractor,

About half this year say they have made no

CLIENT INTELLIGENCE 2013

change since the publication of the strategy a year ago, and even fewer than last year say they have a strategy for reducing costs by 15-20% over the life of the parliament, as the Construction Strategy calls for.

Indeed, much of the forward-thinking

procurement behaviour that the Construction Strategy calls for seems to be led by the private, not public sector. Private sector clients are more likely to make use of both BIM and project bank accounts than public sector ones. However, there are signs of public sector progress on BIM, at least.

The survey repeats last year's finding

that the construction industry will have to continue to bear behaviour from clients, both public and private, that it finds frustrating and potentially damaging. Private sector clients take longer to pay than public ones, but still more than a quarter of public clients take longer than 30 days. Retention payments, a particular bug bear for contractors, are used by more than three-quarters of clients.

Overall, the survey points to clients that

are retaining a ruthless focus on cost and efficiency when they buy construction work, even though (in the private sector, at least) they are more hopeful that the economy will improve enough to allow them to restart projects. Far too many public and private clients – though a slightly lower proportion than last year – still say they struggle to find suppliers with the skills they need, despite intense competition.

Client factfiles

The white paper includes 30 factfiles on

the biggest public and private clients,

excluding the volume housebuilders, who

tend to construct in-house. Including

interviews with the key people responsible

for buying work, these highlight their

upcoming pipeline, and who they

currently work with.

CLIENT INTELLIGENCE 2013

This white paper provides a comprehensive

industry executives referred to in chapter

In the white paper the definition of a

guide to the most important construction

4 was emailed to a targeted group of CEOs

public sector client was taken to include those

clients in the UK, and what they think. It

and senior executives drawn from Building

clients working in industries subject to public

provides an overview of where the work is by

magazine's contacts and from registered

economic regulation, such as social housing,

sector and by region, and a sense of what some

users of the Building website.

energy and rail. These organisations, such as

of the biggest construction firms think about

The private and public/regulated sector

Network Rail, water companies and housing

the state of the market.

client surveys were emailed to a 40,000-strong

associations, are technically private bodies,

The recession has led to a period of

list of clients drawn from the databases of UBM but their spending is largely determined by the

intense pressure on the industry, with

Built Environment, the publisher of Building.

public sector, they are often forced to follow a

public sector workloads falling dramatically.

In addition, the surveys were also emailed to

public sector agenda, and they share many of

The government has continued with its

the database of clients held by pre-qualification the traits of public clients. However, drawing

procurement reform agenda, and private

service ConstructionLine, and the British

the line in this way inevitably becomes hazy at

clients too have responded to the changes in

the margins, and some firms are included as

The survey of the public and regulated sector public sector that may be disputed.

Through a survey of over 300 public and

garnered 208 responses. Of these, 57% were

private clients and a series of interviews with

from what is generally considered the public

3.1.2 top client tables and factfiles

the biggest, this white paper analyses all of the

sector – central government, quangos and local

issues most important to construction firms:

authorities. Of the rest, the biggest single sector The data on individual clients is compiled

what clients value in their supply chain, how

was housing associations, with 49 respondents; from information provided by Barbour ABI, a

they want to buy, and what's likely to change.

the rest came from private companies

leading provider of construction intelligence

In addition we use data from the UK's

in regulated sectors, including 13 from

products, providing UK companies with

leading provider of construction market

infrastructure providers. The vast majority

sales leads, contact data, CRM software and

information, Barbour ABI, to provide a list of

of the respondents procure more than £5m

market intelligence. Barbour ABI is owned

the 50 biggest public and 50 biggest private

of construction a year, with the largest single

by Building's publisher, UBM, and the firm's

clients in the UK, by volume of current work

chunk, 31%, procuring between £20 and £99m

market research team communicates with

– and they're not necessarily who you would

of construction a year. A smaller proportion,

more than 25,000 professionals every month.

think. For the top 30 of these the white paper

11%, procure between £100m and £999m, and

Data has not been independently cross-

drills down further, showing their upcoming

a small elite, 4% procure more than £1bn.

checked with the clients mentioned.

work, and the contractors, QSs and architect

The survey of the private clients generated

The list of 50 biggest clients is based only

that they most like to work with – enabling

around 120 responses, with commercial and

upon current and future schemes. The value

you to benchmark yourself against the most

mixed-use developers making up almost 60%

of schemes is based upon the estimated total

of them. There were over 30 responses from

construction value of "live" projects where

housebuilders, and a further 17 from retail and

the main contract has been awarded in the

leisure sector clients.

last two years, or is currently on site, or is due

The biggest contingent of private clients,

to commence before January 2015. Overall

25%, commission between £100m and £999m

masterplan schemes have been excluded in

This white paper has been compiled through

of work per year. However, a sizable minority

favour of the smaller individual schemes that

a series of interviews and surveys by Building commission very small amounts of work, with

make them up. Schemes on hold have also been

magazine conducted in April and May this

21% procuring under £1m of work per year,

excluded. In addition, the estimated values

year. The market overview consists of a

and another 12% procuring between £1m and

of multi-year framework agreements have

literature review plus the findings of a straw

£4m. Less than 5% of respondents, five in total, been excluded on the basis that the work isn't

poll of construction industry chief executives

commission more than £1bn of work each per

and senior figures.

The detailed profiles of the top 30 clients

is based upon the Barbour ABI list of the

3.1.2 public/private split

50 biggest current clients in the public and private sectors. However, the pure volume

The quantitative surveys were carried out

It is impossible to wholly split the public from housebuilders, many of whom are technically

using the online tool SurveyMonkey.

the private sector in a world where so many

the largest private clients in the industry, have

The straw poll of senior construction

projects are public-private partnerships.

been removed. This is because housebuilders

CLIENT INTELLIGENCE 2013

generally act as main contractor on their

However, like the split between the public

developments, controlling the build directly and

and private sector, the line between a volume

commissioning any specialist subcontractors

housebuilder and a developer is hazy at the

when required themselves. After conversations

margins, and others may draw the line in a

with a number of the housebuilders it was decided

slightly different place.

that Berkeley Group should remain on the list,

For the specific criteria governing the creation

because its construction model is generally much

of each individual dataset on the factfile pages,

closer to that of traditional developers, where it

see the example below:

works alongside external main contractors.

samplE cliENt profilE

1 Name of client

2 The number of current projects being undertaken

3 The number and value of current projects has

been calculated of on the basis of "live" projects where the main contract has been awarded in the last two years, is currently on site or due to commence before January 2015. Overall masterplan schemes have been excluded in favour of the smaller individual schemes that make them up. Schemes on hold have also been excluded. In addition the estimated values of multi-year framework agreements have been excluded on the basis that the work isn't guaranteed. All data on these pages is based on information from Barbour ABI:

4 Profile of client, including type of work, how

it procures, and interviews senior figures where possible

5 The largest of the live projects by value, including

the stage they are at

6 A graph showing the value of construction

contracts let by the client in each of the last five years

7 Projects in the clients' future pipeline, calculated

as those where contracts not yet awarded, and are due to commence after July 2013

8 Lists of the top three contractors, QSs and

architects the client uses. This is based on the total value of the projects upon which the given partner is currently working or has worked in the last five years. See Appendix for total value of projects worked on by key supply chain partners

9 Clients' head office postal address

CLIENT INTELLIGENCE 2013

4/markEt ovErviEw aNd kEy sEctor brEakdowN

Summary – 2012 spend: £98.11bn

period, having recorded a fall in output of

are pockets of growth, with the housing sector

Against a backdrop of continuing retraction

4% in 2012. This is due in part to government standing out in particular, robust recovery

in public spending and a weak economy, the

initiatives such as First Buy and the Funding

will have to wait for wider economic revival

outlook for construction output continues to

for Lending scheme, as well as in the longer

or a return to significant investment by the

be poor. Output in 2012 fell by 8.1% against

term the Help to Buy programme announced

2011 and the forecasts for this year anticipate

in chancellor George Osborne's budget

further reduction, with Experian predicting

statement this year.

a contraction of 2.6%, the Construction

Infrastructure is also seen as a key

Products Association (CPA) 2.1% and Hewes

contributor to the industry's recovery, with

& Associates 3.1%.

transport and energy in particular regarded

2012 spend: £17.02bn

Opinion on when the recovery will start

as growth sub-sectors. Road repair projects

Taking both public and private housing

varies. Both Hewes and Experian expect

announced in last year's autumn statement

together, output fell in 2012 by 7.7%.

further contraction in 2014 of 0.8%, while

should start to have an impact on bottom

According to Experian, however, overall

the CPA anticipates a return to, albeit

lines in the short term and ongoing spending

housing output is expected to return to

modest, growth of 1.9%. However, all three

on the sub-regional Crossrail project – the

growth in 2013 of 1.3%, on the back of a 3%

organisations predict that 2015 will see

largest single construction scheme in Europe

expansion in private housing output and

growth, with Hewes most pessimistic with 1% – continues to provide a vital source of work.

despite further contraction of 5% in public

and the CPA most optimistic with 3.8%.

In addition, wind farm development and

housing. Overall output is expected to grow

Meanwhile, a straw poll of 10 senior

decommissioning works on the UK's nuclear

by 7% in 2014 before falling back to 5% in

executives in the industry carried out for this

power infrastructure continue to provide

white paper demonstrated a split in opinion

valuable revenue streams, although analysts

Leaders in the construction industry

over when stable economic growth will return are pessimistic about the prospects for work

who took part in the straw poll agreed that

to the construction sector. Three of these

on new nuclear facilities contributing much

housing is the sector most likely to bounce

industry leaders believed next year would

to balance sheets in the short term. Indeed,

back quickest. According to those who ranked

see recovery while four opted for 2015 and

Hewes' forecast discounts the Hinkley Point

sources of work for the poll, nine out of 10

a further three were markedly pessimistic,

C project entirely in its calculations.

said they expected privately funded housing

believing that growth would not be seen until

In terms of risk, analysts' warnings range

to be the area of the new-build construction

"2017 or later".

from macro-economic concerns to doubts

market to recover the quickest.

There is a consensus among analysts

over the prospects of complex yet vital

As for publicly funded housing, seven of

that the government's austerity agenda

England-specific policy levers. The possibility these 10 said they expected this sector to be

continues to be the major contributing factor

of further – potentially devastating – turmoil

the most or second-most important area of

to the travails of the construction industry,

in the eurozone cannot be ignored, with the

government spending for their business over

with the CPA reporting that government

ongoing problems in key economies such as

the next two years.

spending on construction in 2013 is likely

Spain and Italy of particular note: if either

to be 18% or £7bn lower this year than

were to default the consequences for the

in 2010. Public sector housing starts fell

continuation of the economic union and the

4.1.1 private housing

by 19% in 2012 and a further fall of 4% is

prospects of its trading partners would be

anticipated in 2013. Both education and

2012 spend: £13.40bn

health spending are anticipated to fall by 15%

From a domestic point of view, analysts

Private housing output fell by 4.3% in 2012

this year, compounding falls of 25% and 19%

point out that the speed at which announced

following two years of growth. Private

respectively in 2012.

infrastructure spending translates into

housing starts fell by 7%, with completions

Asked in the straw poll for their views on

actual work remains a key concern and

increasing 3% boosted by previous years'

the government's spending cuts, seven of

that essential drivers of the repairs and

the senior executives agreed that cuts were

maintenance (R&M) sector, such the Green

However, the evidence from the tail end of

necessary but argued that "growth now

Deal, remain unproven.

2012 and the beginning of 2013 is promising.

depends on capital spending".

Presuming that the coalition government

Orders were up in the last quarter of 2012 and

However, there are still opportunities to be

remains committed to its stated programme

at £2.45bn were the best seen since the third

found. Private sector housing, for instance, is of austerity, the prospects for the construction quarter of 2010. Accordingly, the CPA expects expected to grow each year over the forecast

industry remain sluggish at best. While there

that private housing starts will increase by

CLIENT INTELLIGENCE 2013

8% in 2013, followed by 10% in 2014 and 12%

and the company anticipates additional falls

with nine schemes registered in the first three

in 2015. Similarly, completions are expected

of 10.8% in 2013 and 9.6% in 2014. Output is

months of 2013 and 15 registered in the last

to grow by 4% in 2013, 9% in 2014 and 10% in

expected to stabilise in 2015, at which point

quarter of 2012 and first quarter of 2013.

2015 to reach 128,867 homes.

Hewes expects it to be 20% lower than in 2012

According to the CPA, the growth in

and 42% below the 2010 peak.

4.2.3 other central and local government

private sector housebuilding will be boosted

The straw poll of senior executives,

by the Help to Buy programme, announced

however, revealed a degree of confidence

2012 spend: £2.2bn

in this year's budget and already partially

in the education and healthcare sectors as

Output in this sector, which includes prisons,

up and running. The programme replaces

sources of work with half of the 10 taking

the armed forces' estates and law courts,

two previous schemes – New Buy and First

part arguing that the latter will prove to be

fell by 10% in 2012 following a steep decline

Buy – and provides a mixture of mortgage

the most or second-most important area of

in 2011. According to the CPA, output will

guarantees and equity loans, all on more

government spending for their business over

decline again in 2013 before bottoming out in

generous terms to housebuilders than the

the next two years.

2014. By 2017, the end of the CPA's forecast

previous programmes.

period, output is expected to be £2bn.

However, there has been some movement

4.1.2 public/social housing

in the sector in the last year. The Ministry

2012 spend: £5.26bn

of Justice signed framework contracts worth

2012 spend: £3.62bn

Education output fell by 2.5% in 2011 and 25% about £1bn last year, which should feed

The switch from the old National Affordable

in 2012 due to sharp cuts to the Department

through into work on the UK's prisons estate

Housing Programme to the Affordable

for Education's capital budget. The sector

as well as the court estate. The Defence

Homes Programme, combined with

accounted for 54% of non-housing public

Infrastructure Organisation's framework,

significant reductions in the Department

output last year. According to the CPA,

worth around £400m annually, is currently

for Communities and Local Government's

output is expected to contract by a further

out to tender and is expected to be signed by

(DCLG) capital expenditure budget, led

15% in 2013 and 1% in 2014, before seeing

the end of the year. Finally, the CPA reports

to a fall in social housing starts of 19% to

a return to modest growth in 2015. School

that the MoD is planning to invest £1bn

22,712 in 2012. According to Hewes, the fact

building in the medium term is expected

from its capital budget on accommodation

that the Affordable Homes Programme

to benefit from an additional £1bn capital

for troops returning from Germany in the

allows housing associations to increase

investment announced in December's

medium term.

rents in new developments and thus borrow

autumn statement for free schools and

development finance on the open market to

academies. This has resulted in 78 schools

fund development will not make up for the

having now been selected to share £700m

4.3 private sector building

fall in capital grant. As a result, completions

of direct funding from the Priority Schools

are expected to fall by a further 10% in 2013

Building Programme, with a further 46

2012 spend: £24.94bn

and 4% in 2014 before stabilising in 2015 and

schools to be financed privately. Procurement According to both Experian and Hewes,

returning to growth of 1% in 2016, according

is under way and the first schools are due to

commercial output, which includes both

office and retail development, is set fall

The CPA also anticipates that the DCLG's

significantly over the next two or three years.

decision in August last year to make it

Conversely, industrial output is predicted to

easier for private housebuilders to challenge

increase over the same period.

previously agreed section 106 agreements

2012 spend: £1.5bn

dictating levels of public housing will have a

Output in health construction saw double-

detrimental effect on the sub-sector, although digit decline in both 2011 and 2012. The sector it recognises that the policy move may

accounted for 16% of non-housing output

2012 spend: £6.48bn

ultimately have a positive impact on private

last year. The CPA predicts that output will

Output in the office sector contracted by

contract further in over the next two years,

9% in 2012 and the CPA expects a further

with growth only expected to return in 2015

contraction of 4% this year. Output in 2014 is

followed by 2% rises in both 2016 and 2017, by expected to be flat before starting to rise again

4.2 public sector building

which time output should total £1.3bn.

in 2015 and 2016, by 6% and 7% respectively.

The Procure 21+ framework will be the key

The CPA also reports that the London office

2012 spend: £9.74bn

source of work until the initiative's conclusion market continues to outperform the rest of

According to Hewes, output in public sector

in 2016. According to the CPA, there are

the UK, referencing Google's new £300m

non-housing construction fell by 21% in 2012

currently 120 active Procure 21+ schemes

headquarters in King's Cross – due to begin

CLIENT INTELLIGENCE 2013

work towards the end of this year – and

£1.bn between 2013 and 2015. According to

4.4.3 water, harbours and flood defence

Goldman Sachs' plans for a new HQ in

the CPA, infrastructure output will exceed its

2011 peak in 2015 and continue to rise. The

2012 spend: £2.62bn

public sector currently accounts for 30% of

According to the CPA, water and sewerage

infrastructure output and Hewes expects this

output is expected to fall in 2013, followed

to rise over the next few years, although the

by growth of 2% in 2014. Once work on the

2012 spend: £5.24bn

private sector is still expected to remain the

Thames Tideway Tunnel gets underway

Retail output contracted by 16% in 2012,

dominant force.

the CPA predicts growth of 5% in 2015

largely due to big retailers such as Sainsbury's

and 8% in 2016. Harbours also saw 63%

and Tesco cutting back on their expansion

increase in orders last year. Work continues

plans. Orders in the sector have declined by

on the London Gateway port project in the

75% since 2006. According to the CPA, retail

2012 spend: £5.48bn

Thames Estuary, with the first phase of the

output will contract by a further 10% this

According to the CPA, rail output will

development due to open towards the end of

year before returning to growth in 2014, when increase by 14% in 2013, 10% in 2014 and

output is expected to grow by 1.5% followed

5% in 2015 driven by major London projects

such as Crossrail, the ongoing upgrade of the Thameslink line and the refurbishment and

4.5 repairs and maintenance

development of London Bridge station, as well as increased investment from Network

2012 spend: £35.02bn

2012 spend: £3.28bn

R&M output contracted by 2% in 2012 and

Industrial output grew by about 1% in

Following a fall in the Highways Agency

Experian expects that it will fall by just short

2012, with factories performing much

budget between 2010 and 2012, funding for

of 1% in 2013 before returning to modest

better than warehouses, benefiting from

roads is set to increase from this year. In

growth of around 1% in 2014 and 3% in 2015.

strong investment in the automotive and

total, £415m of motorway upgrade contracts

engineering sectors. Factory output rose

are currently being procured, with work

4.5.1 residential

by 17% to £1.97bn, while warehouse output

scheduled to start towards the end of the year.

declined by 9% to £1.23bn. New orders for

Orders for new road works were 85% higher in 2012 spend: £16.04bn

industrial construction also rose last year by

2012 than in 2011 and the CPA expects output Public housing R&M output increased by

35% to £2.6bn – the highest level since 2008 –

in the sub-sector to be up 8% in 2013 and 10% 0.6% in 2012 following a sharp contraction

based almost entirely on new factory orders,

in 2014 with further expansion to follow.

of 8% in 2011. However, Experian expects no

particularly in the automotive sector.

further fall in 2013 and a return to growth of

4.4.2 energy, airports and communications

1% in 2014 and 2% in 2015. Private housing

4.3.4 leisure and other private sector building

R&M output fell by 6% in 2012, although on

2012 spend: £3.31bn

the back of a less dramatic decline of 1.3% in

2012 spend: £9.94bn

Electricity remains one the few reliable

2011. Experian expects a further contraction

Output in the leisure and entertainment

growth sectors for the foreseeable future with

of 1% in 2013 before a return to growth of 3%

sector declined by 14% in 2012 and now

output rising between 2011 and 2012 despite

in 2014 and 5% in 2015. According to the CPA,

stands at 16% below the average since 2000.

a drop in overall infrastructure output. The

the rise in public housing R&M is accounted

The CPA predicts further contraction of 5%

CPA expects output to rise in the sub-sector

for by the fact that basic repairs have to take

this year followed by a fall of 1% in 2014 and a by 7% in 2013, 10% in 2014 and 15% in 2015.

place under law and that the Decent Homes

rise of 1% in 2015.

However, at the time of writing, the future

programme has been extended to 2015 to deal

of the nuclear build programme remains

with a backlog in work.

in doubt, with negotiations over the "strike

While the CPA says that the impact of

4.4 infrastructure

price" at Hinkley Point C still ongoing.

energy saving initiatives such as the Green

Indeed, Hewes discounts the nuclear

Deal and Energy Company Obligation on

2012 spend: £11.41bn

sub-sector entirely in its forecasts. While

private housing R&M remain uncertain,

Infrastructure output fell by 12% in 2012,

the future of airport development in the

it says that the recent increase in property

largely due to the completion of the latest

South-east – vital to the sub-sector – remains

transactions should drive recovery in the

programme of M25 widening and the

mired in political machinations, there has

short to medium term.

A1 upgrade. However, prospects in the

been some progress recently, with Heathrow

In terms of the straw poll's results, six out

infrastructure sector are relatively good, with

announcing a £3bn investment plan covering of the 10 senior executives who commented

Hewes expecting output to rise by 12% or

2014 to 2019.

on the Green Deal said it would provide their

CLIENT INTELLIGENCE 2013

firm with some work over the next year, with

North-east and London recording 41% and

South-east – which Hewes says will return to

five of these predicting this would be worth

35% falls in orders respectively, while the east a period of relative stability up to 2015 – and

up to 5% of turnover.

of England saw a rise of 92%.

five the Midlands, with other regions scoring

The poll also revealed continuing

While the decline in the North-east

more poorly.

frustration that the government is not more

isn't surprising given the wider economic

actively selling the scheme, with seven out of

performance of the region, the London figure

the 10 arguing that it is not doing enough to

is more startling: orders fell from £3.01bn in

4.7 further market trends

incentivise customers to take it up.

the last quarter of 2011 to £1.96bn in the last quarter of 2012.

The straw poll of 10 senior construction

4.5.2 non-housing

The sharpness of the fall can be accounted

executives suggested that, with the market

for by the drop in infrastructure orders, from

in the UK still tough, firms are increasingly

2012 spend: £18.98bn

£1.19bn in Q4 2011 to £309m in Q4 2012.

looking towards consolidation and work

Public sector non-residential R&M output

Reassuringly, infrastructure orders for Q3

overseas for growth.

fell 1% to £7.2bn between 2011 and 2012,

were almost the exact reverse, with orders of

For example, eight out of the 10 said

according to the CPA. The CPA says that

£312m in Q3 2011 and £1.11bn in Q3 2012. In

they expected the proportion of their firm's

output will fall 3% in 2013 followed by a

other words, the procurement timetables of

turnover that comes from international

further reduction of 1% in 2014. Growth of

a handful of mega-projects such as Crossrail

work to increase over the next two years,

1.5% is expected in 2015, and by the end of

have had a disproportionate effect on the

with South Asia and the Middle East/North

the reporting period in 2017 the CPA expects

statistics for the capital.

Africa seen as the areas of most significant

output to stand at £7.2bn – still 10% lower

That said, Hewes points out that

than the peak in 2009.

commercial orders and education are

In terms of consolidation, a striking six out

In the private sector, non-residential R&M

massively down in London in 2013, and

of 10 said they expected their business to be

totalled £11.7bn in 2012, up 0.7% on 2011.

although the outlook for 2014 and 2015 is a

part of further industry consolidation, either

However, output slipped consistently in each

little better, infrastructure work is peaking,

through a merger, being acquired or acquiring

quarter of the year, with the final quarter

public non-housing orders are down and any

another company.

down 11% on the first quarter. The CPA has

upturn in the commercial sector is unlikely

revised its expectations for the sub-sector in

while so many offices remain vacant.

line with prospects for the commercial sector,

Conversely, new orders were up very

Six out of the 10 industry chief

as well as the wider economy. It now expects

significantly in other regions. The best

executives said they expected

output to be flat in 2013 and for it to grow

performing, the east of England, saw strong

between 2% and 3% each year to 2017.

growth in private commercial, private

their business to be part of further

housing, infrastructure and non-housing

industry consolidation, either

public construction. Similarly, Scotland

4.6 regional spending

through a merger, being acquired

saw orders rise 82% from £734m to

£1.34bn over the same period, with growth

or acquiring another company

in all sub-sectors covered by ONS data apart

Nationally, output fell 9% in the last quarter

from private housing, which contracted

of 2012 compared with the same period of

The poll also revealed a general level

2011, from £26.69bn to £24.21bn. Indeed,

The North-west also reported strong

of frustration with UK government policy

according to Office for National Statistics

growth in orders – up 64% – with private

connected with the built environment.

(ONS) data, output was down in all but one

industrial orders up just short of 900%, from

The exception to the rule appears to be

region of the UK: Wales escaped contraction,

£36m in Q4 2011 to £353m in Q4 2012. The

Whitehall's drive to push take-up of

but didn't see an increase in output either.

region hasn't seen that level of new private

building information modelling (BIM).

Contraction rates varied significantly across

industrial orders for at least a decade. Hewes

Seven out of the 10 questioned said their

the country, with the South-east seeing the

predicts that activity levels will continue to

firms were already using BIM, with the

highest rate of contraction at 16% and the

rise in the North-west up to 2015.

remaining three planning to adopt it in the

east of England the lowest at just over 2%.

Questioned through the straw poll on the

next two years.

However, there are signs that the market

regions of the UK that will offer "significant

may have turned: nationally, orders were 11%

opportunities" for their businesses over

higher in the last quarter of 2012 than they

the next two years, nine out of 10 senior

were in the same period in 2011. Here the

construction industry respondents pointed

regional differences are striking, with the

to London. Six of the 10 also highlighted the

CLIENT INTELLIGENCE 2013

5/cliENt sENtimENt survEy

The sentiment of the construction industry's

Fig 1. How easy do you find it to access project/development finance in the current market?

largest clients is one the most accurate

(Data sample: private sector clients)

gauges of the sector's present state of health and future outlook. This chapter of the

white paper presents clients' workloads and

analyses the corresponding key trends in

how they procure and manage construction,

as well as how they feel the industry engages

with them and how their views have evolved during the past year.

The findings are based on a survey

conducted in May of more than 300 of the

industry's public and private sector clients

and in-depth interviews with leading procuring organisations. The results for 2013

are compared with the information gathered

in a similar survey for our 2012 Client Intelligence white paper. These comparisons

highlight changing trends in payment terms, clients' views on the financial stability of

contractors, the response of public sector

procurers to the government's Construction Strategy and the role of building information

modelling (BIM) in the sector.

This year's survey found that most clients expect access to funds for financing projects to remain constrained in the months ahead. However, many do expect to overcome this

projects, which means that the situation that

challenge, at least to some extent, as they

the industry has faced since the financial

believe projects put on hold will restart and

downturn started in 2008 still holds. When

new projects will begin.

private clients were asked to identify the

When the private client representatives

biggest barrier to commissioning more

were asked how easy they find access to

construction work, the most popular factor

development finance in the current market,

was general macro-economic uncertainty,

the largest group, 48.5%, selected "not easy",

cited by 22.6% (fig 2). This was followed by

with a further 23.2% opting for "not easy at

poor outlook for tenants, cited by 19.4% and

all" – 71.7% in total (fig 1). These results are

a reduced appetite for risk (18.3%). Lack of

worse than last year, when a slightly smaller

bank lending was cited by 15.1% and lack of

proportion, 71%, answered the same question

other funding sources by 17.2% – a situation

with "not easy" or "not easy at all", and a

that most private clients expect to continue,

larger proportion, 20% of the total, said it

with 59.6% of those surveyed anticipating that

was "easy" or "very easy", down to just 15.1%

their ability to access development finance

will stay the same in the next six months.

This year's results show that lenders

Within the private sector, the results for

remain reluctant to finance construction

housebuilders, though a smaller survey group

CLIENT INTELLIGENCE 2013

Fig 2. What do you perceive to be the biggest barrier preventing you from commissioning more construction?

(Data sample: private sector clients)

n General macro-economic

uncertainty 22.6%

n Poor outlook for your business' potential tenants/customers

n Reduced appetite at your organisation for risk in the current market

n Lack of availability of other funding/finance

n Lack of availability of bank lending 15.1%

n High cost of construction

Fig 3. Do you anticipate your business to be more likely to start/restart projects or to put

of 34 respondents, suggested that this area

existing projects onhold in the next six months? (Data sample: private sector clients)

of the sector finds it even more difficult to secure funding. Just over half said it was "not

easy" to access development finance and a

further 23.1% said it was "not easy at all". This

indicates that funding remains challenging for privately-owned housebuilders despite

improved conditions, including many

reporting increased sales and profits in recent months and measures such as the Funding

for Lending initiative bolstering banks' ability to finance their schemes. However, the survey results were a slight improvement on last

year, when 42.9% of housebuilders said access

to development finance was "not easy at all"

and 33.3% deemed it "not easy".

Despite this, overall, private sector clients

have become more confident about the prospects for projects. A majority of 58%

expect their company to either start or restart projects in the next six months (fig 3). This compares with 50% last year. One private

sector client said: "It feels like the global

economy is stabilising and in the UK it seems

that we've avoided a ‘triple dip' recession, so

while we are not expecting a building boom,

the environment is becoming more conducive

for us to take projects forward." Again, the

CLIENT INTELLIGENCE 2013

housebuilders were less optimistic, with just

Fig 4. Do you anticipate your organisation to be more likely to start/restart projects or put

existing projects on hold in the next six months? (Data sample: public and regulated

under half anticipating starting or restarting

sector clients)

projects in the period.

Among the public sector clients surveyed,

n Put projects on hold

the outlook for short-term future spending

n Start/restart projects

has improved marginally compared with

n Neither of the above

last year, even though budgets have been

constrained as part of the government's efforts to cut the national deficit. In 2012 when the survey group was asked how much their construction budget had been cut since before the 2010 Comprehensive Spending Review, 37.1% of respondents said the budget had remained the same or grown. This year, that figure rose to 46.2%. Likewise the proportion that said they had experienced a cut of 10% or more fell from 51.5% to 42.4%.

That said, when asked whether they

thought their organisation was likely to start,

restart or put projects on hold in the next six

months, the numbers were very similar to last Fig 5. Do you expect your budget to improve or get worse before the end of the Spending

year: 37.6% said they expected projects to start Review period? (Data sample: public and regulated sector clients)

or restart, and 22.6% said they expected to put

projects on hold (fig 4).

And an increasing number of public

sector clients believe that, in the longer

term, their capital budgets will be cut further, perhaps reflecting indications from

government that additional budget cuts will

be made in 2015/16. Some 46.2% expect the

cuts they have seen so far to worsen by the

end of the Spending Review period in 2015, up from 37% last year (fig 5). One public

sector client says: "We are undertaking a

major drive to make efficiencies in all areas of procurement and all the indications are that we will have to push this even further in the

"It feels like the global economy

is stabilising and in the UK it seems we've avoided a ‘triple dip'

recession, so while we are not

expecting a building boom, the

environment is becoming more conducive for us to take projects forward"Private sector client

CLIENT INTELLIGENCE 2013

5.2 selection processes

Fig 6. What is your predominant method of procuring contractors? (Data sample: private

sector clients)

The contrast between preferred methods of

n Negotiated contract

procurement in the public and private sectors

n Invited selected contractors

found in last year's survey has remained intact. While private bodies tend to approach

their contractors of choice, public sector

n Public competition

bodies primarily procure from frameworks.

n Select or tender within

In the private sector, clients' predominant

method of procuring contractors remains

n Other long-term partnering

inviting selected companies to compete,

favoured by 50.9% of those surveyed (fig 6). A further 20.7% prefer to negotiate the contract directly with a contractor, without a competitive bidding process. This trend was more pronounced among private housebuilders, of whom 54.8% said their predominant procurement method was

Fig 7. What is your predominant method of procuring contractors? (Data sample: public and

inviting contractors to compete, while 25.8%

regulated sector clients)

opt mostly for negotiated contracts.

What use of frameworks there is among

private sector clients has decreased markedly,

n Using your organisation's

with 42% of respondents saying they made some use of frameworks this year, in contrast

with 50.3% in 2013.

n Using a framework overseen

One representative of a leading private

by a separate organisation

developer interviewed says there is a clear

rationale behind invitation-only tendering. He says: "We invite a select group of firms to bid for our projects. It is a costly business for a contractor to produce a good, detailed tender, so if you pick the right people in advance and give them a one in two or three chance of winning the job you are more likely to get a considered approach from the contractors."

Public sector clients, which are restricted

by regulations from using such closed

This was the most popular reason cited for

are even less likely to use OJEU, presumably

selection processes, tend to use frameworks

use of frameworks, whereas clients said

because their resources and expenditure

rather than the other main route open to

OJEU still required greater amounts of time

are particularly constrained. Among those

them of tendering through the Official

and higher costs.

procuring £1m-4m worth of construction

Journal of the European Union (OJEU).

One council procurer criticises OJEU

work per year, only 13.6% use the journal

Of the public sector clients surveyed,

because he believes it leads to smaller

predominantly, while 54.5% use their

51.6% said their predominant method of

businesses being excluded from contracts:

organisation's own framework and 27.3%

procurement was to use their organisation's

"We like to employ small firms and we see

opt for another body's framework. Among

own framework; a further 18.6% use another

this as our responsibility but most don't have

those procuring less than £1m annually, none

organisation's framework (fig 7).

the bid teams needed to get through the

reported mainly using OJEU.

Only one in four (24.8%) predominantly

OJEU process. The problem for us is we have

Indeed, use of frameworks in the public

use OJEU. These percentages, which are

more than 2,000 lease holders so when they

sector appears to be increasing. Some 83.8%

broadly the same as last year's findings,

are involved in a contract by law we have to

of the sector's respondents said that they

reflect the belief that frameworks result in

use OJEU so that they can have a say in the

made at least some use of frameworks,

improved co-operation with contractors, due

selection process."

compared with 81.6% in 2012. The trend looks

to the longer term nature of the relationship.

Public bodies procuring smaller amounts

set to become even more pronounced because

CLIENT INTELLIGENCE 2013

45.2% said they expected their organisation's

Fig 8. Do you make use of any of the following in your relationship with your supply

chain or suppliers? Tick all that apply. (Data sample: public and regulated sector clients)

use of frameworks to grow.

Electronic tendering, championed by

the previous Labour government as a more efficient approach to the bidding process

n Project bank accounts

within the public sector, appears not to have

n Retention payments

seen increased take-up in the past year. Less

n Electronic tendering

than half (44.9%) of respondents in 2012

n Factoring or reverse

said they made any use of electronic

tendering and this year the percentage is

n Rebates, incentive

payments or any other

Prequalification, which can save time

for clients and money for suppliers, is

form of money back

also used relatively sparingly. This is

despite the availability of methods to make prequalification less time-consuming such

as the Constuctionline service and the government's introduction in 2010 of PAS91,

a standardised prequalification form that means suppliers only have to go through the

process of inputting basic details, such as insurance arrangements, once. Despite the fact that PAS91 was updated in April to make

it more user-friendly, only 37.7% of public sector clients said they used the standard or any other form of prequalification.

As tendering remains extremely

Fig 9. Do you make use of any of the following in your relationship with your supply chain

competitive, the clients interviewed reported

or suppliers? Tick all that apply. (Data sample: private sector clients)

that they are concerned by below-cost bidding, echoing the views expressed in

n Project bank accounts

last year's interviews. This year one public

n Retention payments

sector client representative said: "We are

n Electronic tendering

very sensitive to below-cost bidding. We

try to tackle it by selecting based on quality

n Factoring or reverse

rather than prices and really questioning the

contractor about whether they can deliver

n Rebates, incentive

what they say they will for the price – and

payments or any other

hopefully getting them to realise what would

form of money back

be a more sensible price. In many cases

we have not selected main contractors and specialist trades because their bids looked too

low. We are spending government money so

"In many cases we have not

selected main contractors and specialist trades because their

bids looked too low"Public sector client

CLIENT INTELLIGENCE 2013

Fig 10. What types of contract do you use most? (Data sample: private sector clients)

we don't want to put people out of work."

n Lump sum design and build

As was the case in 2012, this year's survey

found that both public and private sector

n Construction management

clients predominantly use lump-sum

n Other partnering

design-and-build contracts. Both types of

body have also reduced their use of target-price contracts, which share the risk of cost overruns between the client, contractor and supply chain. With lump-sum contracts placing more risk with the contractor, the trend in contracts demonstrates that in the current market, where workloads are much reduced, clients hold the balance of power.

Of the private sector clients surveyed,

56.6% said they use lump-sum design-and-

Fig 11. What types of contract do you use most? (Data sample: public and regulated

build contracts, which was similar to last

year's finding that the contract form was used by 57.7%. The use of target-price contracts,

n Lump sum design and build

meanwhile, has reduced from 12.1% last year

to 9.4% in 2013 (fig 10).

However, private sector clients appear to

opt to retain some risks in certain cases. The

n Construction management

second most common contract form used

n Other partnering

in the private sector remains construction

management, where the client appoints the contractor and then separately contracts the trades, which are then the client's contractual risk. This year 21.7% said they use construction management contracts, which was in fact an increase on 2012, when 16.1% reported using the form.

One private sector procurer says: "We

use design-and-build contracts above all because, as long as you have a complete package of information on which you can contract, giving the contractor control over the design is usually more efficient. But our procurement method varies depending on the nature of the work. In the case of a pre-let scheme, construction management may be

and other partnering contracts (14.2%)

away from target-price contracts though. One

better suited to meeting fast-changing tenant has remained fairly unchanged. However,

representative of a local authority, which has

the use of target-price contracts has fallen

been using partnering contracts for several

In the public sector, although lump-sum

dramatically, suggesting again a shift in the

years, is about to introduce the contract form.

design-and-build is the predominant form of

balance of power in favour of the client. In

He says: "We would like to transfer more risk

contract, there has been a decrease in their

2013, just 11.3% of public bodies reported

to the contractor, but we know that this is

use, with 40.4% using them now compared

using the contract form compared with

something you have to pay for and we [the

to 45.1% in 2012 (fig 11). The use of

procurement department] have to answer to

construction management (11.3% in 2013)

Not all public sector clients are moving

our political masters." Introducing target-

CLIENT INTELLIGENCE 2013

Fig 12. What are your standard payment terms for contractors?

price contracts "feels like a halfway house

(Data sample: private sector clients)

between where we are and transferring 100%

of the risk to the contractor".

Marked changes in payment practices were

revealed by the survey– and not all of the news was discouraging for contractors.

Among the private sector respondents,

standard payment times have polarised over the past year, with far fewer clients paying in the previously standard 15-29 days. Many

clients are actually paying far more quickly, though others are of course lengthening

payment times. The largest proportion, 40.8%, now pay in 30-59 days (fig 12).

In a further sign of increased client power

and correspondingly challenging conditions

for suppliers, 77.6% of private clients still

make use of retentions (fig 9). Moreover,

this form of delayed payment has increased

slightly compared to last year, when 76.4% of

private clients said they used it.

Meanwhile, standard payment times have

shortened in the public sector. The highest

Fig 13. What are your standard payment terms for contractors?

proportion of clients (43.2%) said they pay

(Data sample: public and regulated sector clients)

in 15-29 days, whereas last year 47.7% used this payment period. However, this year a

significant 18.2% said they now pay in 0-14

days, compared with 8% in 2012. Fewer

clients' standard payment terms are 30-59

days: 32.8% used this timeframe last year but

in 2013 the percentage has fallen to 25.0%. This appears to reflect heightened awareness in government of the industry's calls for "fair

payment" (fig 13).

Less encouragingly for contractors, the use

of retentions has remained constant in the

public sector. Both this year and last year, our

survey found that the practice was used by

77.6% of respondents at public organisations (fig 8). This comes despite government initiatives designed to reduce retentions.

However, it is probably too early to see the

impact of one of the most significant of

these: the launch In April of a suite of NEC3

contracts including fair payment provisions.

There remains relatively slight use of

mechanisms that could ease financial

pressure on contractors and the supply

CLIENT INTELLIGENCE 2013

Fig 14. What qualities are most important to you in selecting a contractor? Rank from 1-7 in order of importance where 1 is the most

important. (Data source: private sector clients)

Proven build quality

Financial stability

Relationship with the supply chain

Ability to innovate in delivery

Ability to offer sustainable construction

Ability to work with BIM

chain in both the private and public sectors.

of contractors than they were a year ago.

"We try to guard against the

Project bank accounts are used by 23.5% of

This appears to be a consequence of clients'

problem by doing vigorous checks

private sector clients and 11.2% of public

limited budgets and increasing insolvencies

before we work with firms and

clients – figures that changed little from last

among contractors. When clients were

year's survey. Factoring or reverse factoring,

asked to consider which qualities are

then remaining vigilant, but

mechanisms that can support suppliers' cash

most important to them when selecting

sometimes these things can come

flow, were even less popular, used by just 3.5% a contractor, the financial stability of the of private clients and 3.4% of public sector

contractor and their price were found to

respondents (figs 8 and 9).

have grown in significance – although a track

Private sector client

Meanwhile, the use of rebates, incentive

record in good quality construction remained

payments or any other forms of money back

the top priority for clients.

from suppliers to keep them on tender lists

Of the private sector clients surveyed,

has declined, possibly reflecting continued

proven build quality remained the most

third most important qualities to clients.

pressure on clients to reform payment

important factor for them when choosing a

However, the financial stability of contractors

practices. In the private sector, 20.5% of

contractor. It registered an average priority

has now become the number one factor for

clients reported using such incentives in 2012 ranking of 2.3 when respondents were asked

30.7% of respondents, compared with 25.7%

but this year the percentage has fallen to

to rank qualities from 1-7, with 1 being the

17.6%. In the public sector, the numbers have

highest (fig 14). This compared with an

One private sector client says: "We have

fallen from 13.5% of clients in 2012 to 7.8%

average ranking of 2.03 last year. However,

seen a number of contractors going bust

price was closer to being as high a priority,

in the past year and this has become an

being rated at an average of 2.53, with 70%

extremely important concern for us. On one

saying it was either the most important or

project we had seven suppliers go under,

5.5 Qualities sought

second most important factor this year,

which was very challenging. We try to guard

compared to 68% last year.

against the problem by doing vigorous

The survey found that clients have become

As with last year, price and financial

checks before we work with firms and then

more concerned with the financial health

stability were respectively the second and

remaining vigilant, but sometimes these

CLIENT INTELLIGENCE 2013

Fig 15. What qualities are most important to you in selecting a contractor? Rank from 1-7 in order of importance where 1 is the most

important. (Data source: public and regulated sector clients)

Proven build quality

Financial stability

Relationship with the supply chain

Ability to innovate in delivery

Ability to offer sustainable construction

Ability to work with BIM

things can come out of the blue."

major headache."

on last year's sentiment, when only 38.3%

The public sector has seen price become a

When asked how easily they are able to

said it was "easy" and 57.1% deemed it "not

higher priority, registering an average priority find the qualities and skills they want in

easy" or "not at all easy".

rating of 2.5, compared with 2.76 last year.

the sector, 61.1% of the private sector clients

Although the reason for this change in

The contractor's price was this year cited

surveyed said they found it either "not

sentiment is not entirely clear, it may be

as the most important factor by 38.2% of

easy" or "not at all easy", despite the current

because public bodies are now procuring less

clients as opposed to 27% last year. However,

buyer's market. This view has become more

and perhaps simpler work, as the government

proven build quality remains the most

prevalent, as it was held by 57.3% last year.

continues its drive to cut spending. If public

important factor when choosing a contractor,

One representative of a private client

bodies are procuring fewer jobs this could

registering an average priority ranking of 2.41. organisation cites intense price competition.

mean they have fewer problems finding the

Financial stability has marginally decreased

He says: "The depressed prices in the UK

right suppliers. Indeed, the findings from the

in significance, achieving an average priority

are putting off a lot of European companies

public bodies surveyed procuring more than

ranking of 2.94, but remaining clearly in third – they feel it's not worthwhile working here

£1bn of work per year – although a smaller

at the moment. This is quite worrying

group – do support this. This group reported

For some public sector clients, suppliers

because the type of projects we do often

more trouble finding the skills and qualities

that are small and medium sized enterprises

require technical competency only found

they need, with some 75% saying it was either

(SMEs) present a particular worry. One

in mainland Europe. We are particularly

"not easy" or "not at all easy".

representative of one of the sector's largest

concerned about the appetite for working

clients says: "We can award an SME a

in the UK of cladding and curtain walling

contract but the question is whether they will

be able to borrow the money to finance it.

Public sector clients are slightly more

We don't hold retentions and we use projects

optimistic about their ability to find the

Revealingly, the survey also highlighted the

bank accounts but we are still acutely aware

qualities and skills they need. Some 42.6%

contractors' skills and qualities that clients

that these smaller firms can become insolvent said it was "easy" and 46.6% said "not easy"

see as less important. These included the

and then present our supply chain with a

or "not at all easy". In contrast to the private

ability to offer sustainable construction,

sector respondents, this was an improvement

CLIENT INTELLIGENCE 2013

which was again the sixth most important

Fig 16. Have you made use of BIM in any of your projects?

factor in selecting a contractor – in other

(Data source: private sector clients)

words, less important than all other priorities

except BIM. Sustainability was cited as

the most important attribute sought in contractors by only 11.5% of private clients

and 9.5% of public sector respondents.

Among public sector clients, the result

was not significantly different from 2012,

but among private clients the percentage

choosing it as their first priority had slipped

from 14.3%. This supports the view expressed

by many in the industry that sustainability

has slipped down the agenda in commercial construction during the downturn as financial concerns have become paramount.

Not all private sector clients express this

view, however. One says: "We have never let

sustainability slip off our agenda and it has been a concern for us for many years." He

adds: "We are switching our focus, though, and looking increasingly at the embodied

carbon of our buildings rather than just the

carbon emitted while the building is in use."

However, the ability to innovate in delivery

seems to have become more important for both public and private sector clients over the last year. It moved from being the fifth most important factor when selecting a contractor to the fourth, achieving an average rating

Perhaps supporting both of these findings,

However, when asked whether BIM would

of 3.48 for public clients and 3.6 for private

72% of private and 54% of public sector

become more important to the construction

clients – making it more important than the

respondents said they had not undertaken

projects they commission over the next two

relationship with the supply chain. However,

any procurement on the basis of whole-life

years, a significant 55% of private sector

the factor remained a long way behind the

costing rather than up-front construction

clients said yes, up from 46.4% last year.

top three – price, quality and stability – and it

cost, a big increase on last year's finding.

BIM is in fact already being used increasingly

is clear that, while growing in importance, the However, a significant proportion of both

by clients, the survey found. In 2012 one

ability of contractors to innovate is not a top

types of client (47.5% of the private sector and third of private clients had used BIM on

priority for many clients.

56.2% of the public sector) indicated that they any projects, but in this year's survey 46% believe that whole-life costing will become

said they have used the system (fig 16). The

important to their organisation over the next

housebuilders, however, were lagging, with

some 63% saying they had not used BIM.

"We have never let sustainability

The ability to work with BIM was by far

The public sector, despite the message

the least important factor when choosing a

from government, is behind in its use of BIM,

slip off our agenda and it has

contractor, the same result as last year. Just

although it has grown here too. In 2012, 18.9%

been a concern for us for many

4.8% of private and 7.4% of public sector

of the public sector respondents said they

years. We are switching our focus, clients cited this as their top priority.

had used BIM but this year the percentage

The results suggests that despite the

has risen to 33.6% (fig 17). Perhaps more

though, and looking increasingly government's endorsement of BIM,

surprisingly, when asked whether BIM would

at the embodied carbon of our

including stipulating that level 2 BIM be

become more important to the construction

used on all public sector projects by 2016, the

projects they commission over the next two

approach has yet to become a major priority

years, 50.4 % of public sector respondents

Private sector client

said yes, down from 54%. One public sector

CLIENT INTELLIGENCE 2013

client representative working in housing says: Fig 17. What use have you made of BIM in any of your projects?

"BIM is largely untested in housing so we

(Data source: public and regulated sector clients)

want to move cautiously and make sure there is demonstrable added value. Some building

types are less complex than some others,

which reduces some of the advantages of BIM

in the construction process."

While the use of BIM is not strongly

prevalent among public sector clients

procuring above £1bn a year, with only 14.3% saying they had used the system, of those

procuring £20m to £999m a year, around 42%

said they had worked with the technology. One client says: "BIM can be an enormous

help in the move from development to asset management, providing an already-populated

stock management tool, which is vital when you will be holding the asset for 30-plus

years. Perhaps more importantly, it provides

a platform for collaborative working between

client, developer, contractors and trades."

5.7 government policy

Overall the survey found that clients would like more clarity from government on the policies that affect construction. The clients were asked whether, if the government gave a clearer and more consistent message that it will prioritise policy changes that aim to tackle the threat of damaging climate change, it would affect whether or how they invest in their built assets. Some 61% of private and 62% of public sector clients answered yes. Around the same number also said they thought the government should send a clearer message that it will prioritise policy changes that aim to tackle climate change.

A significant proportion of private

sector clients were also sceptical about the government's policy of cutting spending quickly to reduce the UK budget deficit. When asked if cutting spending to reduce the deficit would improve business confidence for the year ahead, a majority of 58% said it would have the opposite effect. Just 14% thought it would improve confidence, 18% said they did not know and 10% said the policy makes no difference (fig 18).

However, the private clients surveyed were

CLIENT INTELLIGENCE 2013

less united in terms of how they would like to

Fig 18. Do you feel that the government's policy of cutting spending quickly to reduce the UK

see the situation resolved. Only 49% said the

budget deficit is improving business confidence for the year ahead?

(Data source: private sector clients)

government should increase capital spending to boost confidence and construction activity, even if that meant additional public

n Improving confidence

borrowing. In contrast a significant 32%

n Worsening confidence

said that the government should stay on its

n Government spending makes

The government's Construction Strategy,

published in May 2011, is still failing to register a wider influence on public sector clients. In 2012, 54.3% of clients said the strategy had not changed the way they procure construction work, 17.9% said it had but only marginally and 5.8% said it had significantly. This year the percentage that said the strategy had not changed their approach fell slightly to 49.3% (fig 19).

Only 3.5% said it had changed the way they

procure significantly, with 23.2% saying it had changed their approach only marginally.

And when the public sector clients were

Fig 19. Has the publication of the government's Construction Strategy in May 2011 changed

asked whether they had a strategy for

the way you procure construction work? (Data source: public and regulated sector clients)

reducing construction costs over the life of

the current parliament, as required by the

Construction Strategy, some 46.1% said

that they did not. Only 28.4% said they

were targeting such cost reductions.

Meanwhile, several public sector client

representatives interviewed said they are reducing construction spending in any case,